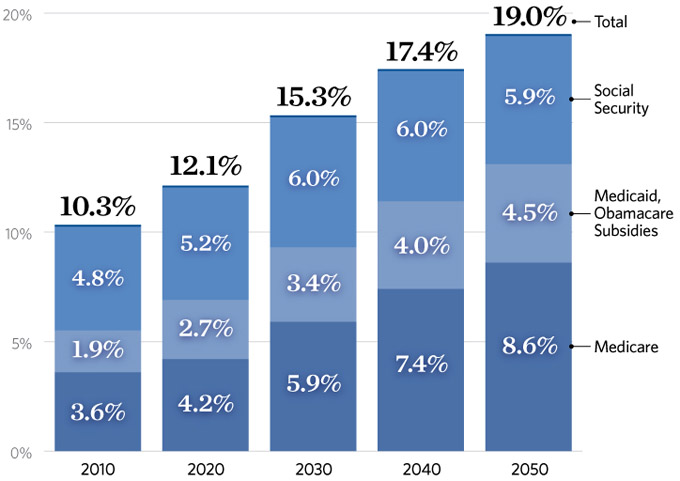

Social Security, the popular retirement program, will soon go bankrupt if nothing is done to change the trajectory of this program. Social Security, first introduced in 1935 by President Franklin Delano Roosevelt, supplies older Americans who are not working with much needed income. The system operates as a “pay as you go” program. This term simply means that current workers’ payroll taxes go into the Social Security Trust Funds. Thus, current beneficiaries will earn their retirement benefits based upon the current work force (not what they paid in throughout their lives). However, that simple model has become more and more difficult to maintain, as approximately 10,000 Americans retire from the workforce every day (according to www.house.budget.gov).

In 1990, there was approximately a proportion of three workers paying into the program and one retiree collecting benefits. Subsequently, though, that ratio has worsened and now approximately two workers are paying into the program and one retiree collecting benefits. (These stats provided by Samir S. Soneji and Gary King in the journal Demography.)

Another strain on this popular program has been an increase in individual lifespan since 1935. The program must ergo pay their benefits for a longer duration of time without reciprocal compensation. Also, the older one gets, the more proportionally more healthcare you need. Therefore, Social Security has many problems that cannot continue to go unnoticed in Washington D.C.

But there are many easy solutions that can help this program survive past its projected death in 2033, according to Social Security Actuaries. The government should increase the eligibility/retirement age for Social Security. By increasing the retirement age for Social Security to 70, one would allow the program more time to prepare for the next wave of retirees. Also, it would force folks to stash away more money for their retirement. The program presently begins providing full benefits at 66, and that threshold is scheduled to eventually move to 67.

Secondly, we should institute a system that shifts the formula for cost of living adjustments of Social Security to the “chained CPI.” “Chained CPI” is a measure of inflation that has the possibility of slowing down Social Security benefits. It assumes that as the price of one good goes up, you’ll buy a cheaper good, thus limiting the amount of money you would need to purchase those goods. On the other hand, a current measure of inflation assumes that you’ll just buy the same good, raising your cost-of-living faster.

Washington should also promote means testing, which would allow lower income seniors to face less of the brunt of the proposed reforms. Means testing would force wealthier beneficiaires to pay higher premiums to keep the program solvent. Also, since critics of “chained CPI” usually cite the impact on low income seniors, means testing would be able to mollify some of their concerns.

In conclusion, politicians in Washington DC must be willing to put Social Security changes on the table. In 2011, the Obama Administraion supported “chained CPI” as mentioned above. Over the last 3 years, the Republican-controlled House of Representatives has passed numerous budgets that dealt with entitlement programs. Let’s merge these efforts together to achieve the elusive “grand bargain”, a mix of spending cuts, health reforms, and revenue increases.